Portfolio Design Strategy, Refilling Our Cash Buckets, and Listening to Experts

This week’s newsletter is a story about not knowing what you don’t know and a how-to idea for those who like bucketing. If this appeals to those who manage their own money, that’s great. But my real intention is to give you a better understanding and language to have more productive conversations with your Financial Advisor.

I’ll start with the story: When I was in practice, a lovely woman was referred to me. She was divorced, not working (she had stayed home to raise the children), and her ex-husband had stopped paying his contractually committed monthly maintenance. While she was far from destitute, the money she had was all she would ever have unless she went to work.

She came to me asking for an income portfolio. This is a specific portfolio design that foregoes growth in favor of consistent income and preservation of the principal. Normally, it’s used for large portfolios that are intended for inheritance or donation.

”Do you know what an income portfolio is?” I asked. “No, but that’s what I want,” she replied. I asked her if I could design a more productive total return portfolio for distribution, a well-structured, diversified portfolio producing both growth and income. She said that would not be acceptable. She wanted an income portfolio and nothing else would do.

Her other challenge was that her ex-husband had failed to keep his promise to pay for their daughter’s upcoming wedding. I do not know, not having met the daughter, how she felt about this. What I do know is that Mom wanted to make good on the commitment to fund the event. I asked if there was a way to provide a gift to her daughter a few years down the line, which would permit her portfolio to grow and compound more. She was adamant that she wanted to help her daughter pay for the wedding now. Of course, the price tag on the wedding grew as planning took place.

In the end, we parted ways. This woman did not want to be told that her plan—to use an income portfolio and also fund her daughter’s wedding—would not leave her enough money to fund her lifestyle to 100. I explained that I did not want to be second-guessed regularly by whomever told her to create an income portfolio. (There was definitely someone chirping in her ear; she indicated as much.)

That’s okay, by the way. Two things (at least) are required for a good client/advisor relationship: trust and a “good fit” between the parties. It’s important to be able to pick a fight (nicely) when there’s a fight that needs to be had. But what is sad about this story is that this woman was so insistent I employ a particular portfolio design that was not going to help her achieve her goals without knowing why she was asking for it. My fingers are crossed that everything worked out well for her.

If you employ an expert, listen to the expertise first (even though you may not agree with it).

As an aside, while her early lump sum distribution was the main reason for running out of money, there’s a lot of damage done to would-be-happy retirements in favor of protecting principal. This is one of those permission to spend problems, wherein people don’t enjoy retirement because they won’t spend their money, even if they have enough to last to age 100.

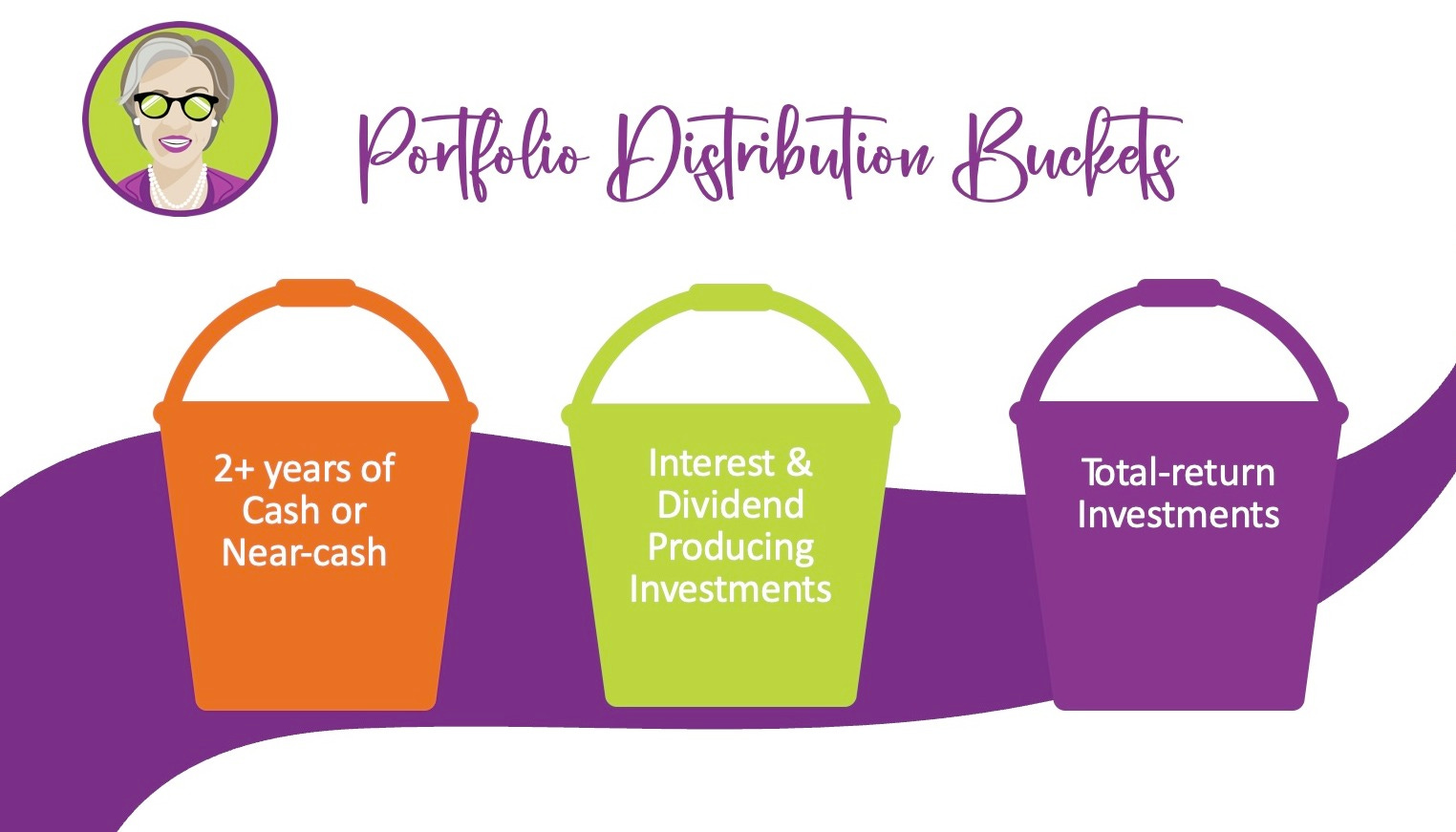

Anyway, producing income, preserving principal, and adopting a total-return strategy are NOT entirely at odds when it comes to creating portfolio distributions. They’re part of the bucket strategy.

That brings me to the how-to:

Using the Bucket Method, your first bucket should hold two or more years of cash or near-cash to use so that you never have to take money from a down market.

Your second bucket should hold interest and dividend producing investments, the distributions from which will refill the first bucket.

Your third bucket, to be invested for total return, supplies lump-sum distributions and, when rebalancing, replenishes buckets 2 and 1.

These may be virtual buckets or actual accounts. That’s up to you. But it’s important to realize that what got you here won’t get you there, so to speak. Your portfolio may have compounded beautifully with low-cost index funds and ETFs. But if they don’t produce a dividend payment, you may have to swap them out as you design your distribution. For example, the only way to take a distribution from Berkshire Hathaway stock is to sell your Berkshire Hathaway stock. It’s ideal for building wealth, but NOT for distributing it, because they intentionally do not pay a dividend. Thus, Berkshire Hathaway belongs in the third bucket, the total-return bucket.

To the extent that your portfolio contains bonds, bond funds, and dividend income producing investments, the first step to refilling your cash buffer might be as simple as turning off your automated reinvestment. As you’ve received dividends and interest from your holdings, they’ve been automatically buying more shares of those same holdings. But you can ask your Advisor to turn that off at any time. This will show you how much income your portfolio already produces. Then, in order to produce more income, you can finesse some of your investments.

Armed with how much income your portfolio produces and how much of your cash bucket you deplete quarterly, the difference between those two numbers is approximately how much income you’ll likely need until you update your inflation calculation. Reduce that by your guaranteed income sources (pension, Social Security, annuities) and you have the amount of income you want to produce.

There are proven and reliable dividend-producing stocks and income-producing funds that you can add to your portfolio in exchange for some pure growth assets. The modern market is always innovating with new products. And, with an ageing population and increasing positive correlation between stocks and bonds (they used to be opposites; now it’s iffy) there are new ways to achieve income.

Recently, I swapped some Vanguard S&P 500 EFT (VOO) for JP Morgan Equity Premium Income (JEPI). JEPI was created in 2020 and pays a monthly dividend. Unlike the passive VOO, it’s an actively managed ETF that writes covered calls for income. I found it by using ChatGPT to produce a list of monthly income funds. Then I asked a friend who manages a $2 billion portfolio, and he said it’s now his go-to for income.

There’s nothing wrong with VOO. It’s lots of people’s favorite low-cost, high-performing ETF. Mine too. Except, it won’t produce the dividends required to replenish my cash bucket. And I’m not ready to start taking distributions in earnest. (I may not be for some time.) But, as an experiment, I thought it was cool to have an instrument that produced income without interfering with my asset allocation. I am trading one S&P 500 tracker for another. Thus, my large-cap asset class remains intact.

Whether it’s designing a fresh portfolio strategy or seeing what new products are available to execute a portfolio strategy you’re already comfortable with, nobody knows everything about the market. Don’t be stubborn. If you employ an expert, listen to their expertise. You’ll also find that most people who are experts defer to others’ expertise to stay up to date. #WeRescueOurselves

Reading: The Bucket Approach to Building a Retirement Portfolio, Christine Benz, Morningstar

Let me know what you think and subscribe here.

Membership includes access to me for Q&A, member Zooms, my office hours to work on your financial and longevity model, and Madrina Molly’s library of articles and mini-courses.

Good news: Our new website is almost ready!

Copyright Madrina Molly, LLC 2025

The information contained herein and shared by Madrina Molly™ constitutes financial education and not investment or financial advice.

Sherry Finkel Murphy, CFP®, RICP®, ChFC®, is the Founder and CEO of Madrina Molly, LLC.

I wish I understood this stuff a little better. Thanks for the lesson, it sounds like it makes sense.